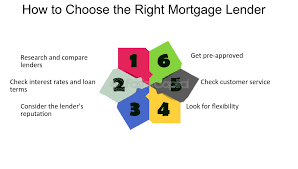

Selecting the right mortgage can significantly impact your financial future. Here are some tips to help you make the best choice:

Assess Your Financial Situation

Understanding your current financial status is the first step. Evaluate your income, expenses, savings, and credit score. This assessment will help you determine how much you can afford to borrow and repay comfortably.

Consider the Loan Term

Mortgages typically come with various loan terms, such as 15, 20, or 30 years. A shorter loan term means higher monthly payments but less interest paid over the life of the loan. Conversely, a longer loan term offers lower monthly payments but more interest paid overall. Choose a term that aligns with your financial goals and budget.

Evaluate Interest Rates and Fees

Interest rates can vary significantly between lenders. Shop around and compare rates to find the most competitive option. Also, consider other fees associated with the loan, such as origination fees, closing costs, and any prepayment penalties. These fees can add up and impact the overall cost of the mortgage.

Understand the Different Loan Types

Each mortgage type has its advantages and disadvantages. For instance, fixed-rate mortgages offer stability with consistent payments, while adjustable-rate mortgages may offer lower initial rates but come with the risk of increasing payments over time. FHA and VA loans provide specific benefits for certain borrowers. Thoroughly research each type to determine which suits your needs best.

Get Pre-Approved

A mortgage pre-approval gives you a clear picture of what you can afford and makes you a more attractive buyer. It shows sellers that you are serious and capable of securing financing, which can be beneficial in competitive markets.

Consult with a Financial Advisor

A financial advisor can provide personalized advice based on your unique situation. They can help you understand the long-term implications of different mortgage options and guide you towards the best decision.

Managing Your Mortgage

Once you have secured a mortgage, managing it effectively is crucial for maintaining financial health. Here are some tips:

Make Extra Payments

If possible, making extra payments towards your mortgage principal can reduce the loan’s term and the total interest paid. Even small additional payments can make a significant difference over time.

Monitor Interest Rates

Interest rates fluctuate over time. If rates drop significantly, consider refinancing your mortgage to take advantage of lower rates. This can reduce your monthly payments and the overall cost of the loan.

Maintain Good Credit

Your credit score affects your mortgage terms and rates. Continue to manage your credit responsibly by paying bills on time, keeping balances low on credit cards, and avoiding unnecessary debt.

Budget for Maintenance and Repairs

Owning a home comes with additional expenses for maintenance and repairs. Create a budget for these costs to avoid financial strain when unexpected issues arise. Regular maintenance can also help preserve your property’s value.

Build an Emergency Fund

Having an emergency fund is essential for covering unexpected expenses, including potential mortgage payment issues. Aim to save three to six months’ worth of living expenses to ensure financial stability.

The Impact of Mortgages on Your Financial Future

A mortgage is not just a loan; it’s a significant financial commitment that can impact your overall financial health and future. Here’s how:

Building Equity

As you pay down your mortgage, you build equity in your home. This equity represents ownership and can be a valuable asset for future financial needs, such as funding a child’s education, starting a business, or covering retirement expenses.

Tax Benefits

Homeowners can benefit from various tax deductions related to mortgage interest and property taxes. These deductions can reduce your taxable income, resulting in significant savings. Consult a tax advisor to understand how these benefits apply to your situation.

Wealth Accumulation

Real estate is often considered a solid investment. Over time, property values tend to appreciate, potentially increasing your wealth. Owning a home can be a key component of a diversified investment portfolio.

Financial Discipline

Managing a mortgage requires financial discipline. Regular mortgage payments can instill good financial habits and improve your overall financial management skills.

Long-Term Stability

Owning a home provides long-term stability compared to renting. Fixed mortgage payments offer predictability, whereas rent can increase over time. Homeownership can provide a sense of security and belonging.

Common Mortgage Mistakes to Avoid

Navigating the mortgage process can be challenging. Avoid these common mistakes to ensure a smoother experience:

Not Shopping Around

Failing to compare rates and terms from multiple lenders can cost you thousands of dollars over the life of the loan. Take the time to shop around and find the best deal.

Ignoring the Total Cost

Focusing solely on monthly payments can be misleading. Consider the total cost of the mortgage, including interest and fees, to understand the true financial commitment.

Overextending Your Budget

It’s easy to get carried away with a higher loan amount. Stick to a budget that allows you to comfortably afford your mortgage payments without sacrificing other financial goals.

Not Reading the Fine Print

Mortgages come with various terms and conditions. Carefully read all documents and understand the implications of each clause. If something is unclear, seek clarification from your lender or a financial advisor.

Skipping the Pre-Approval

House hunting without a pre-approval can lead to disappointment if you find a home you love but can’t secure financing. Getting pre-approved provides a clear budget and demonstrates to sellers that you are a serious buyer.

Mortgage Refinance: Key Considerations

Refinancing your mortgage can be a strategic financial move, but it requires careful consideration. Here are some key factors to keep in mind when contemplating refinancing:

Reasons to Refinance

There are several compelling reasons to consider refinancing your mortgage:

- Lower Interest Rates: If interest rates have dropped since you took out your original mortgage, refinancing could reduce your monthly payments and the total amount of interest paid over the life of the loan.

- Shorten Loan Term: Refinancing to a shorter loan term can help you pay off your mortgage faster, saving money on interest, and allowing you to build equity more quickly.

- Access Home Equity: Cash-out refinancing enables you to tap into your home’s equity for significant expenses such as home renovations, debt consolidation, or major purchases.

- Switch Loan Types: Moving from an adjustable-rate mortgage (ARM) to a fixed-rate mortgage can provide stability with predictable payments, protecting you from future interest rate hikes.

- Remove PMI: If you originally put down less than 20% and are paying private mortgage insurance (PMI), refinancing can eliminate PMI if your home has gained sufficient equity.

Costs Involved in Refinancing

Refinancing is not without costs. Be aware of the following expenses:

- Closing Costs: These can include appraisal fees, loan origination fees, title insurance, and more, typically amounting to 2-5% of the loan amount.

- Prepayment Penalties: Some mortgages have prepayment penalties for paying off the loan early, which can offset the savings from refinancing.

- Points: You may have the option to pay points upfront to reduce your interest rate. While this can save money in the long run, it requires a higher upfront cost.

Break-Even Point

Calculate the break-even point to determine if refinancing makes financial sense. This is the point at which the savings from the lower interest rate offset the refinancing costs. For example, if your closing costs are $3,000 and you save $150 per month, your break-even point would be 20 months ($3,000 / $150).

Refinancing Requirements

Lenders have specific requirements for refinancing:

- Credit Score: A higher credit score can secure better terms and lower interest rates. Generally, a score of 620 or higher is needed, but 740 or above will qualify for the best rates.

- Loan-to-Value Ratio (LTV): Lenders prefer an LTV of 80% or lower, meaning your home’s value should be at least 20% higher than your mortgage balance.

- Debt-to-Income Ratio (DTI): A lower DTI, ideally below 43%, is favorable as it shows you can manage your current debts and the new mortgage payments.

Understanding Mortgage Rates

Mortgage rates significantly affect your monthly payments and the total cost of your loan. Here’s what you need to know about how they are determined and how to secure the best rate:

Factors Influencing Mortgage Rates

Several factors influence mortgage rates, including:

- Economic Indicators: Rates are affected by broader economic factors such as inflation, employment rates, and the Federal Reserve’s monetary policy.

- Credit Score: Higher credit scores typically result in lower interest rates as lenders see you as less of a risk.

- Down Payment: A larger down payment reduces the loan amount, which can lead to a lower interest rate.

- Loan Amount and Term: Larger loans and longer terms usually carry higher interest rates due to the increased risk for lenders.

How to Get the Best Mortgage Rate

- Improve Your Credit Score: Pay bills on time, reduce debt, and avoid opening new credit accounts before applying for a mortgage.

- Compare Multiple Lenders: Don’t settle for the first offer. Compare rates and terms from multiple lenders to find the best deal.

- Lock in Your Rate: Once you find a favorable rate, lock it in to protect against rate increases before closing.

Fixed vs. Adjustable Rates

Deciding between a fixed-rate and an adjustable-rate mortgage depends on your financial situation and market conditions:

- Fixed-Rate Mortgages: Offer stability with consistent payments, ideal if you plan to stay in your home long-term.

- Adjustable-Rate Mortgages (ARMs): Typically start with lower rates that can adjust periodically. These can be beneficial if you expect to sell or refinance before the initial rate period ends.

Impact of Mortgages on Personal Finances

Taking on a mortgage is a significant financial decision with long-term implications. Here’s how it can impact your finances:

Building Wealth Through Homeownership

Homeownership is a common way to build wealth over time. Each mortgage payment reduces your principal balance and increases your equity. As property values appreciate, your investment grows, contributing to your overall net worth.

Tax Benefits of Mortgages

Mortgages come with potential tax benefits, such as deducting mortgage interest and property taxes. These deductions can lower your taxable income, providing significant savings. However, tax laws change, so consult with a tax advisor for the latest information.

Balancing Mortgage Payments and Savings

While paying down your mortgage is important, it’s also crucial to balance these payments with saving for other financial goals, such as retirement, emergency funds, and education. A well-rounded financial plan ensures stability and preparedness for the future.

Managing Financial Risks

Mortgages carry risks, including the potential for market downturns that can affect property values and interest rates. Diversifying your investments and maintaining an emergency fund can help mitigate these risks.

Conclusion

Understanding and managing mortgages is vital for making informed financial decisions and securing your financial future. From selecting the right mortgage to navigating the refinancing process and leveraging tax benefits, knowledge empowers you to make choices that align with your goals and financial well-being. By avoiding common pitfalls and staying informed about market trends, you can ensure that your mortgage serves as a powerful tool for building wealth and achieving long-term stability.